Sunk costs

Sunk costs are costs that have already been incurred in the past and that nothing we do now or in the future can affect.

These costs won’t affect the decision making and economic analysis at present and in the future. A typical example for sunk cost in the oil and gas industry is the cost that has been spent on drilling a well. That well may have been producing for many years by the time a decision must be made for whether the well should be abandoned, but in this situation, drilling cost is sunk cost and it’s irrelevant for the analysis. A similar concept is applicable to revenues from previous years and all its tax and commitments that have been paid.

Opportunity cost

Opportunity cost(link is external) is hidden or implied cost that is incurred when a person or organization forgoes the opportunity to realize positive cash flow from an investment in order to take a different investment course of action. A typical opportunity cost example is to sell a property or keep and develop it. If an investor forgoes realizing a sale value positive cash flow in order to keep and develop a property, an opportunity cost equal to the positive cash flow that could be realized from selling must be included in the analysis of development economics.

Also, as explained before, minimum rate of return used to analyze a project is actually the opportunity cost of capital (not the cost of borrowing money). Minimum rate of return is the return on capital that could be invested in other projects. Consequently, minimum rate of return is equivalent to opportunity cost of capital.

Break-even analysis

Break-even analysis includes calculating one unknown parameter (such as annual revenues, product selling prices, project selling prices, and break-even acquisition costs) based on all other known parameters under the condition that costs break even the profits. When calculating and analyzing the unknown parameters for after tax considerations, it is very important to apply the after tax values. For example, minimum rate of return applied to calculate after tax NPV should be the rate corresponding to after tax analysis of the project.

Example 9-4

Consider a fairly old producing machine. As a manager you have two alternatives:

Sell the machine: You can sell the machine in the market now for $500,000 with zero book value and pay the tax of 35%.

Keep the machine: You can decide to keep the machine but an overhaul cost of $800,000 is required to repair and improve the machine. The overhaul cost is depreciable from time 0 to year 3 (over four years) based on MACRS 7-year life depreciation with the half year convention (Table A-1 at IRS(link is external)). After overhaul, the machine would be able to produce and generate equal annual revenue for three years (year 1 to 3). In the end of year 3, salvage value of the machine will be 100,000 dollars (zero book value). The operating cost of the machine for year 1, 2, and 3 will be $300,000, $400,000 and $500,000.

Assuming 35% income tax rate and after-tax minimum ROR of 18%, calculate the minimum annual revenue that the machine has to generate to break-even the selling with NPV of keeping the machine.

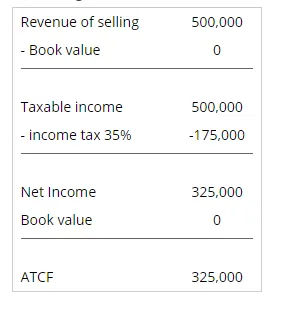

Selling the machine